By Drs. Justin Baker and Chanheung Cho and Clarisse Owens, North Carolina State University and STEPS Center

In February 2026 the White House issued a new Executive Order to ensure an adequate domestic supply of elemental phosphorus and glyphosate to support national defense interests. This EO came as a surprise, and it came just a few months after another surprise announcement – the inclusion of phosphate rock in the final 2025 critical minerals list produced by the US Geological Survey. The final list of selected critical minerals is determined based on an analysis conducted by the USGS, which considers both economic contributions of raw materials and their respective supply chain risks. Interestingly, this report ranked phosphate rock as a relatively low risk, low economic contribution mineral compared to other minerals that are key to information technology and energy systems such as lithium and cobalt. Adding intrigue to the decision to include phosphate rock in the critical mineral list, a recent CRS report suggested that phosphate rock was included due to a special request from the US Dept. of Agriculture. Phosphorus-based fertilizer is ingrained into our food systems, and changes in this supply chain have a large impact on domestic agricultural operations that seeps into food accessibility and availability concerns.

So should phosphate rock be considered a critical mineral? Prior to its inclusion, there was certainly political momentum pushing for phosphate to be added to the list. Senator Tom Tillis introduced a bill to the 118th Congress (S.3956) to include phosphate on the final list of critical minerals while other Senators continued this push in 2025. Further, a recent analysis of critical minerals and materials for the US energy system by the Department of Energy (DOE) identifies phosphorus as likely to shift from low to moderate supply risk between 2025 and 2035, providing some additional policy justification for its inclusion.

A deeper dive into phosphorus supply chains (in the U.S. and globally) suggests potential vulnerabilities to food and industrial systems that warrant careful consideration and planning to avoid future disruption. We discussed some of these concerns in a recent publication on phosphorus supply chain disruptions, others have discussed similar concerns here, here, and here (note: some of these articles are behind paywalls and we cannot provide access). But we revisit that discussion here to provide additional context on supply chain vulnerabilities that are somewhat unique to phosphate rock and its associated end products.

First, phosphorus-derived products are important in several economic sectors – not just agriculture. The overwhelming majority (>95%) of phosphate consumption in the U.S. goes to wet processing of P-based fertilizers such as diammonium phosphate (DAP), monoammonium phosphate (MAP), and triple super phosphate (TSP). Phosphate rock is processed into phosphoric acid and is then used to produce fertilizer products that are critical to the global food system. While phosphoric acid serves as the “bridge” between phosphate rock and most fertilizers, it is also used in other important industrial applications, including:

- Metal treatment and industrial metal processing (e.g., pickling, rust removal, and corrosion protection);

- Food and beverage industries (acidulant in sodas, preservative, pH control, baking powders, dairy applications); and

- Water treatment and detergents,

Outside of phosphoric acid, phosphorus-derived chemicals include elemental phosphorus (tied to glyphosate and defense applications), as well as compounds used in flame retardants and other niche industrial markets. While the proportion of phosphate used in the energy system is currently small, it is possible that lithium iron phosphate (LFP) batteries could play an important role in future energy transitions in the U.S. and elsewhere.

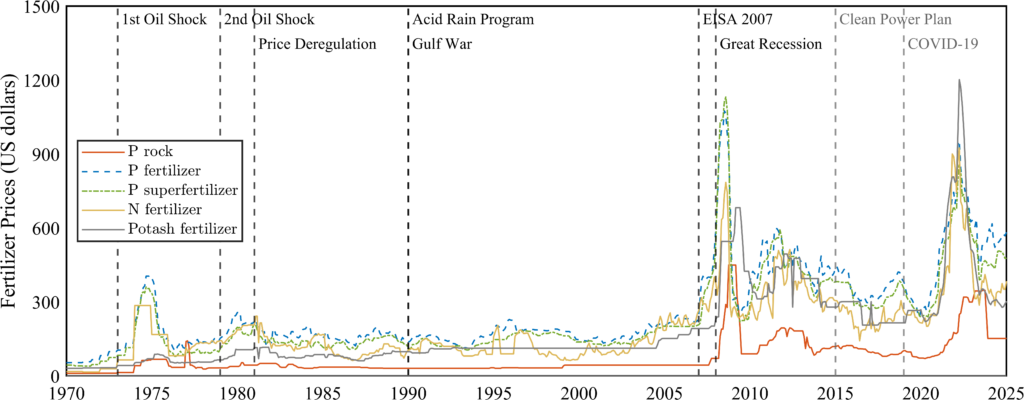

Second, phosphate rock and related fertilizer markets have exhibited high levels of market volatility over the past two decades. The following figure shows monthly (nominal) prices for key fertilizer commodities dating back to 1970, using World Bank price statistics. The figure shows how key global events or energy policy actions have corresponded to both temporary and lasting price effects. Following price spikes of both the Great Recession (2008) and COVID-19 pandemic, prices for most fertilizer commodities experienced increased volatility and sustained higher prices. Despite falling slightly, prices for phosphate rock and most P fertilizers never quite recovered to lower (pre-Recession) market price conditions unlike other energy and agricultural commodities.

Even in real terms, prices for phosphate rock and phosphorus-based fertilizers have increased slightly since the early 2000s, despite technological improvements and expanded global trade. These market conditions are partially explained by growing demand for phosphorus fertilizers in growing agricultural markets. But are these trends also capturing a scarcity signal? While there are adequate supplies of proven phosphate rock globally, scarcity signals in P rock and related commodity markets may be capturing the supply constraints driven by the limited number of key supply points for P rock globally. Mineral reserves are concentrated in a few regions such as Morocco, China, Russia, the United States, and others, giving those regions considerable market power and creating potential supply bottlenecks.

Third, with growing demand for phosphorus-derived products globally, supply gluts caused by centralized resource stocks and production systems are likely contributing to relative market volatility and rising prices in recent decades. Global fertilizer markets have shown susceptibility to recent global shocks, but unlike energy commodities, price recovery in fertilizer markets has been affected by trade policy decisions. The COVID-19 pandemic and subsequent conflict in Ukraine resulted in protectionist trade policies in some key supply regions that limited both raw material and fertilizer availability in the global market. There is now early evidence that the conflict-driven closure of the Strait of Hormuz is limiting trade in already strained fertilizer markets, suggesting a continued bumpy road for global phosphate and fertilizer markets. The near- and long-term implications of these compounding events remain to be seen, but as the last six years have shown, higher fertilizer prices and price volatility could adversely impact U.S. and global food systems.

Nominal monthly commodity prices for phosphate rock and fertilizer commodities from the World Bank Commodity Price report. Data accessed in February 2026 from this link. Figure compiled by RES-Lab andSTEPS postdoctoral scholar Dr.Chanheung Cho.

So while this piece does not directly advocate for critical mineral designation for phosphate rock, federal efforts to recognize the importance of this resource and efforts to stabilize its supply may indeed be warranted given observed market disruption over the last two decades, general upward mobility on phosphate and fertilizer prices, and the critical role of phosphorus across the agriculture and industrial sectors. Inclusion of phosphate rock offers opportunities to improve supply chain resilience in the US through incentives to expand resource extraction and industrial processing to increase the domestic supply of P-based products. Critical minerals that are relevant to national defense receive priority status in federal projects for investment and scalability. Critical mineral entities can receive support through public-private-partnerships, tax credits, and reduced regulatory hurdles to expand production.

Importantly, reduced regulatory barriers and related incentives that may come with critical mineral designation raise important sustainability concerns – expanded mining and industrial operations come with environmental risks and could undermine efforts to improve phosphorus sustainability (e.g., interventions to reduce P losses to surface waters). These potential tradeoffs warrant careful consideration moving forward.

If (in the case of phosphate) critical mineral designation emphasizes increased supply chain resilience, this designation could facilitate the implementation of complementary policies that support sustainable phosphorus transitions. On the demand side, designation could include innovations in P use efficiency – technological breakthroughs that reduce the overall derived demand for phosphorus fertilizers in US cropping systems could ameliorate the net impact of supply chain disruption.

On the supply-side, designation could support incentives for alternative fertilizers sourced from phosphorus secondary recovery and reuse (e.g. P capture from human waste streams or wastewater treatment plants, or direct capture and removal from surface water systems). The potential for circularity within secondary recovery of phosphorus exists within industrial byproducts from operations in mining and fertilizer production.

Though not a widespread practice, there is potential to embed environmental considerations that promote circularity in the form of reuse and recycling initiatives in critical mineral offtake agreements and other incentives. There is precedence for critical mineral designation supporting recycling and reuse programs. Successful policy initiatives for the energy sector (i.e. the $1B Critical Mineral Fund from the Department of Energy) have allocated a large portion of government funds to the development of recycling, refining, and recovering critical minerals.

Academic discussions in the U.S. and in Europe, where phosphorus was included on Critical Raw Minerals List in 2020, include how governance intended for sustainability can frame policies that scale technologies for P recovery, improve nutrient management on farms, and utilize market instruments to reduce barriers for experimentation with recovered products. A shift in the framing of critical recycling and reuse should be captured as an opportunity for market growth and scalability for a mineral like phosphorus that has consistent, if not growing, demand.

We (researchers affiliated with the STEPS Center) will continue to track market and policy developments post-critical mineral designation. Leveraging critical mineral status in the U.S. to facilitate new incentives for phosphorus recovery and reuse, improvements in P-use efficiency, and increased use of legacy P could serve the dual purpose of increasing the resilience of phosphorus supply chains to global shocks while improving environmental outcomes.

Opinions expressed here do not necessarily reflect those of the Sustainable Phosphorus Alliance or its members.